Board of Assessors

Andy Myers, Chair

Timothy Dunn, Clerk

Laura Lafreniere, Member

Assessor Clerk

Melvyn Hook

Office Hours

Hours: Tuesdays 11am to 3pm

Also available by appointment; email [email protected] or call the office at (413) 354-6318 to make an appointment.

Meetings

Meetings are held as needed.

Contact the Assessors

Office: (413) 354-6318

Send a message to the Assessors →

Tax Rate for 2026

Tax Rate Residential: $18.06 per 1,000

Tax Rate Commercial: $18.06 per 1,000

Tax Rate Personal Property: $18.06 per 1,000

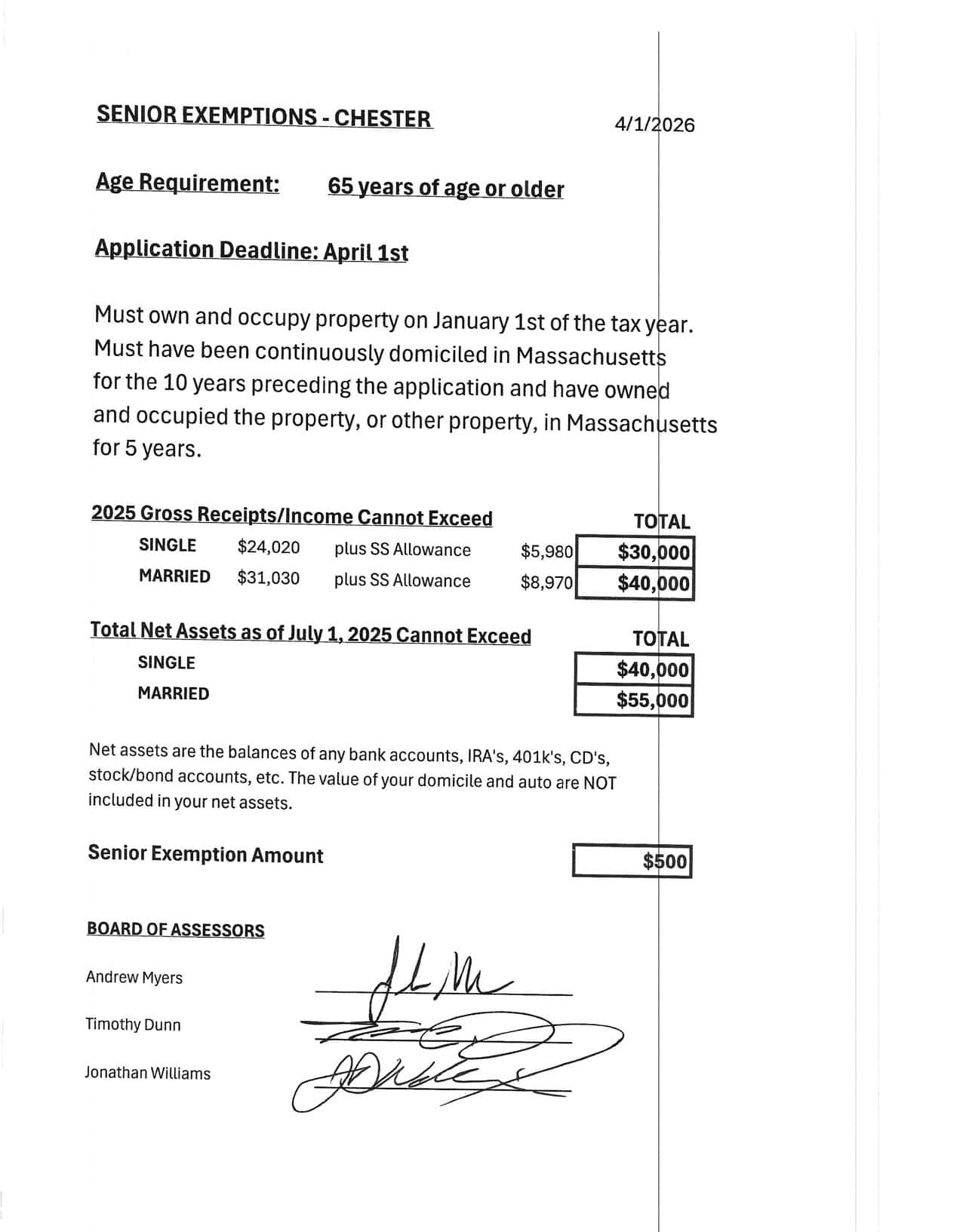

Senior Exemptions (click to view)

General Information

WHAT ASSESSORS DO

Assessors are elected or appointed locally in Massachusetts’s cities and towns. The Assessors are required by Massachusetts Law to list and value all real and personal property. The valuations are subject to ad valorem taxation on the assessment roll each year. The “ad valorem” basis for taxation means that all property should be taxed “according to value”, which is the definition of ad valorem. Assessed values in Massachusetts are based on “full and fair cash value”, or 100 percent of fair market value.

Assessors are required to submit these values to the State Department of Revenue for certification every three years. In the years between certification, Assessors must also maintain the values. The Assessors review sales and the market every year and thereby reassess values each year. This is done so that the property taxpayer pays his or her fair share of the cost of local government, in proportion to the amount of money the property is worth, on a yearly basis rather than every three years.

In addition, the Department administers the Motor Vehicle Excise taxes.

WHAT ASSESSORS DO NOT DO

The Assessors do not raise or lower taxes. The Assessors do not make the laws, which affect property owners. The Massachusetts Constitution requires that direct taxes on persons be proportionately and reasonably imposed. In addition, the Declaration or Rights, Part I, Article 10, requires each individual to bear his fair share of the public expenses.

The Assessors are required to annually assess taxes in an amount sufficient to cover the State and Local appropriations chargeable to the Town. These taxes assessed will include State and County assessments which have been duly certified to the Board and local appropriations voted by the Town Meeting.

The Assessors Office has nothing to do with the total amount of taxes collected. The Assessor’s primary responsibility is to find the “full and fair cash value” of your property, so that you may pay only your fair share of the taxes. The tax rate is determined by all the taxing agencies within the community, and is the basis for the budget needed to provide for services, such as schools, roads, fire, law enforcement, etc. The tax rates are simply those rates, which will provide funds to pay for those services.

WHAT IF I DISAGREE WITH THE ASSESSED VALUE OF MY PROPERTY?

If your opinion of the value of your property differs from the assessed value, by all means go to the Assessors’ office and collect pertinent data to support your opinion. The Board of Assessors will be glad to answer your questions about the reassessment procedures. When questioning the assessed value, ask yourself these questions:

• Is my data correct?

• Is my value in line with others on the street?

• Is my value in line with recent sale prices in my neighborhood?

Keep in mind what’s important: recent sale prices, condition, neighborhood, building area and lot area are the most critical factors in the valuation process. There is a variety of information available to help you determine whether your assessment is fair and equitable. The Assessors will be happy to assist you.

If, after discussing the matter with the Assessors and researching the assessments of comparable properties within your area, a difference of opinion still exists, you may appeal your assessment to the Board of Assessors by filing an abatement application.

Chester is on quarterly tax bills: the first two bills are preliminary tax payments based on your prior year’s taxes. The notice of third payment, referred to as the “actual tax bill” is when the filing period for abatement applications commences. The third tax bill (actual bill) is usually issued the end of December. The application must be filed with the Board of Assessors no later than February 1. The information regarding filing an abatement or exemption application is also on your tax bill. The application must be on file in the Assessors’ office and not just postmarked on that date. You are appealing your assessment, not your taxes. You must pay your taxes pending your appeal. If your application is not timely filed, the assessors cannot by law grant an abatement or exemption.

The Assessors have three months to take action on your abatement application. If it is approved, you will receive a certificate indicating the amount of the abatement. If your tax bill has a balance to be paid, the abatement will credited to your next payment. If your tax bill is paid in full, you will be sent a refund check. If your application is denied, you will receive a notice of denial. You may call and set up an appointment to meet with the Board of Assessors to discuss the reason for the denial. Or you may appeal to the State Appellate Tax Board (ATB) within three months of the date of the Assessors decision. They are located at 100 Cambridge Street, Boston, MA 02108 (617-727-3100).

The assessment date is June 30, as it affects your ownership status. The property is legally assessed to the owner as of January 1, but make sure you get a bill! You may be entitled to file an application for abatement if you dispute your value. Or, as the owner of property July 1, you may be entitled to file an application for one of the statutory exemptions that are available.

WHAT TYPES OF EXEMPTIONS DOES CHESTER OFFER?

A variety of exemptions is available to reduce the property tax obligations for certain qualifying taxpayers: Disabled Veterans, Elderly Persons and Blind Persons. Exemption applications can be sent to you from the office or are available online here:

• Disabled Veterans

• Seniors/Elderly

• Blind Persons

Contact the Assessors Office if you have any questions on the requirements for these exemptions and to find out if you qualify.

The qualifying date for these exemptions is July 1, the first day of the fiscal year. You must own, occupy and otherwise qualify for the exemption as of July 1. Applications must be filed within three months from the mailing of the actual tax bill. It is advised that the taxpayer file as early as possible.

HOW CAN I APPEAL?

If you are not satisfied with the action taken by the Board of Assessors regarding your request for abatement or exemption, you have the right to appeal to the State Appellate Tax Board, 100 Cambridge Street, Ste. 200, Boston, MA 02114. If you have any questions or would like to request an application for appeal, you may also call the Appellate Tax Board at 617-727-3100, or visit their website at www.mass.gov/atb.